Asia’s ultra-high net worth boom could fuel family office scene

2024-08-22

Global private banks dominant in Asia, including UBS, HSBC and JPM, may need to dedicate more resources to serve family offices in the region. These clients’ portfolios tend to have home biases, with sizable allocations to China and the rest of Asia. More new ultra-high net worth individuals could be created in the Asia-Pacific region over the next five years than in other regions.

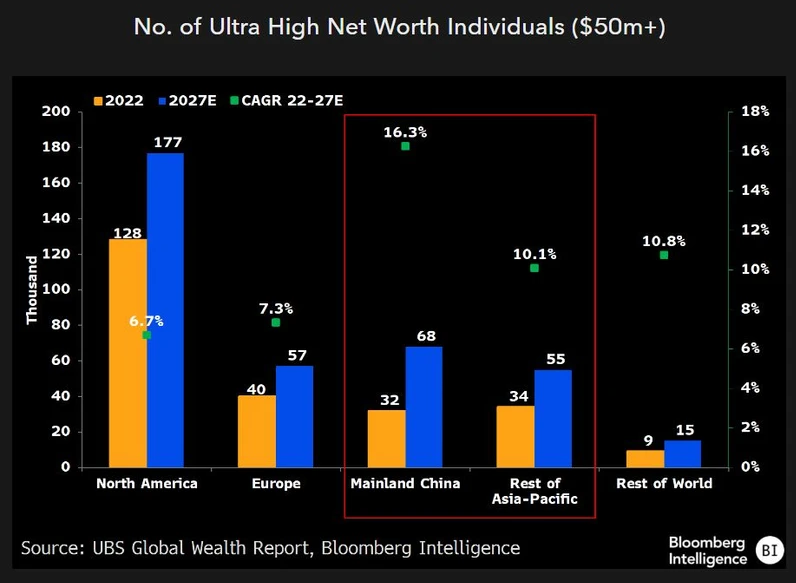

Asia-Pacific region to lead wealth creation

The rise of family offices in Asia will be supported by the region’s growing affluence and need to preserve wealth through intergenerational transfers. The number of ultra-high net worth individuals in the Asia-Pacific region with over $50 million of wealth could grow 13% annually to reach 123,000 by 2027, accounting for a third of the world’s total, according to UBS’s Global Wealth Report. Mainland China could overtake Europe by 2025 with over 50,000 ultra-high net worth individuals, we calculate, based on UBS data. The family-office space in Asia is still young compared to the US and Europe as most wealth in the region is self-made and concentrated in the first or second generation. But offices are becoming more sophisticated and diverse.

Asia’s family offices more conservative

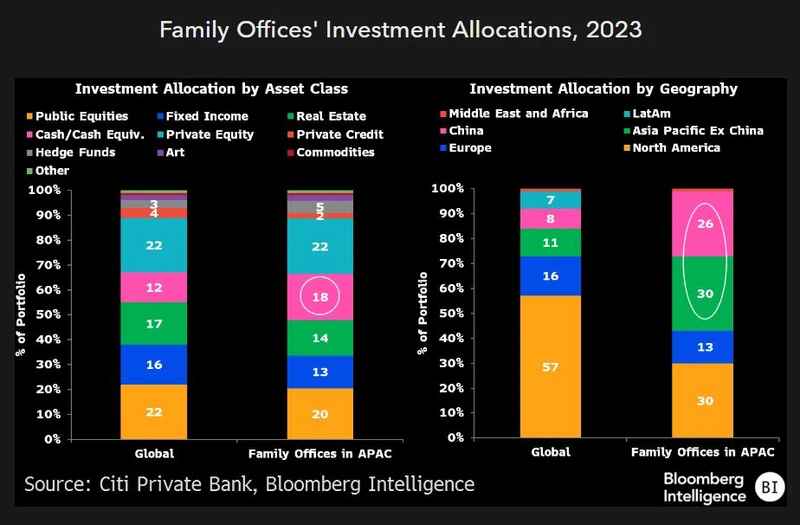

Family offices based in Asia tend to take a relatively cautious approach, with 18% of portfolios held in cash and cash equivalents compared with 12% for family offices globally, according to a survey by Citi Private Bank. Geopolitics is the biggest worry, while rising inflation and the risk that global financial-system instability could hit markets and the economy are also key concerns. Asian offices are heavily invested within the region, in line with the home bias of family offices globally. The survey showed China accounts for 26% and the rest of the Asia-Pacific region 30% of portfolios.

Family offices are more exposed to alternative assets than other types of investor, reflecting expectations for higher returns, due-diligence capabilities and an ability to bear illiquidity risk due to longer-term investment horizons.

Family offices’ rising risk tolerance

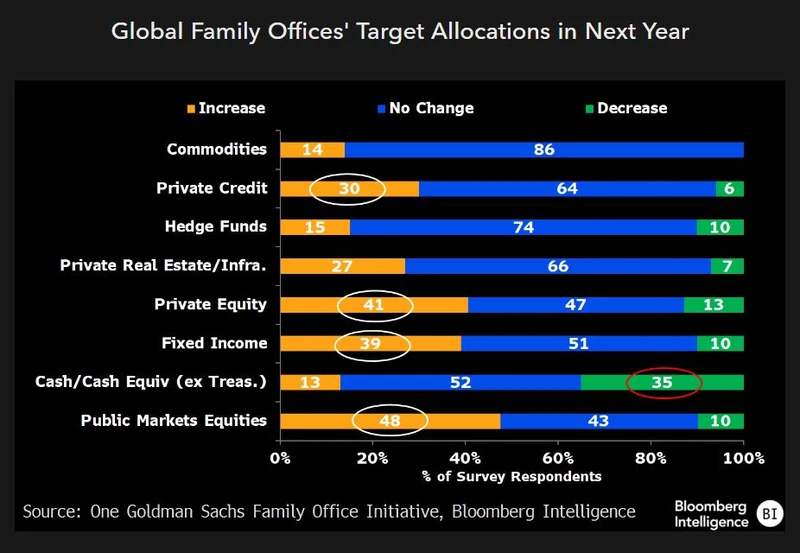

Risk appetites of family offices might rise over the next 12 months as many look to trim investment allocations to cash and cash equivalents, and increase investment in listed equities, fixed income, private equity and private credit, according to a Goldman Sachs survey published in March. Average duration of portfolios could lengthen as central bank policies normalize.

Family offices’ demand for alternative assets, which provide returns not correlated with public markets and diversification benefits, could rise further from already outsized allocations. Exposure to private credit, which is small, could offer family offices stable cash flows amid economic uncertainty, seniority in the capital structure and enhanced yields.

Geopolitics could drive regional diversification

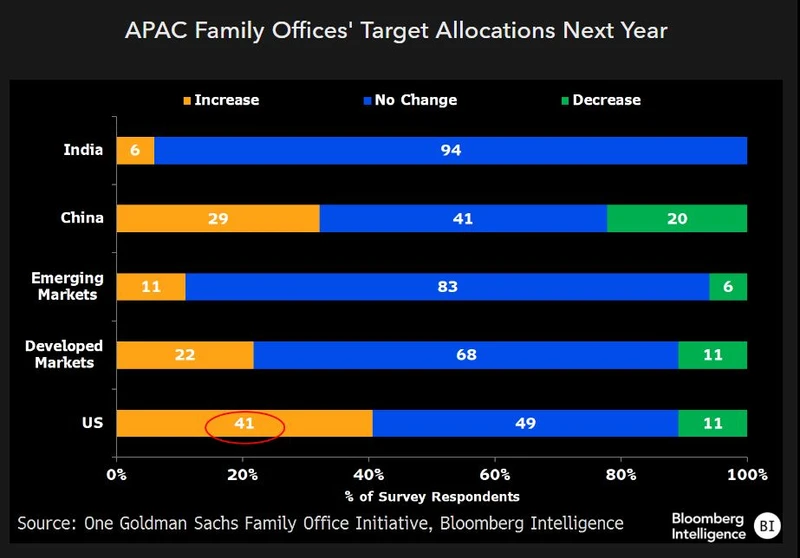

Family offices in the Asia-Pacific region could look to increase their target strategic allocations to US investments and stay cautious on India and other emerging markets, potentially reflecting a preference for safe havens in an uncertain macroeconomic environment, and a focus on regional diversification driven by concern over Sino-US tensions, according to the Goldman Sachs survey. Yet the view on China appears divided with 29% of respondents in Asia planning to increase and 20% planning to decrease their allocations to the country.

China’s once-a-decade reforms could cause short-term pain, particularly for small caps, but drive healthier development of its financial markets in the long term. Family offices can explore opportunities that leverage advanced technology and innovation such as health care and biotech.

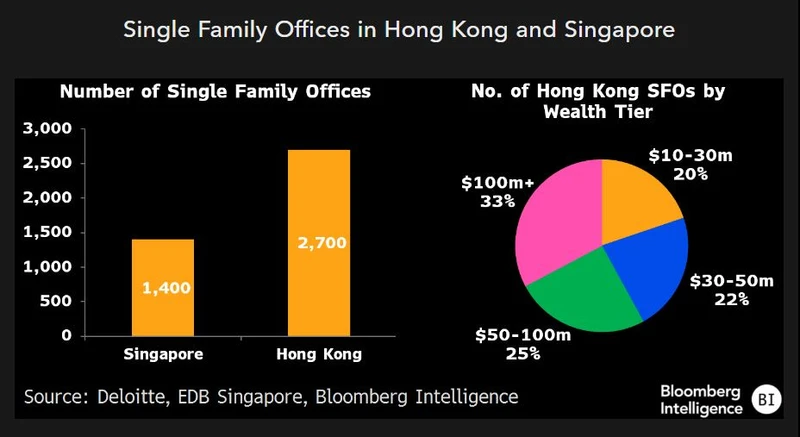

Hong Kong’s lead over Singapore could widen

Hong Kong had about 2,700 single family offices (SFOs) in 2023, according to a Deloitte survey commissioned by the Hong Kong government. About a third of SFOs in Hong Kong were set up by ultra-high-net-worth individuals with more than $100 million and another 25% with $50-$100 million in assets. In Singapore, there were 1,400 SFOs in 2023. Hong Kong numbers are estimates because no regulatory pre-approval is required to set up an SFO, unlike in Singapore where SFOs need approval from the Monetary Authority.

The Hong Kong government’s preferential policies and tax breaks for SFOs contrasts with Singapore’s tighter anti-money laundering and tax rules as well as lengthier application processing times.

Sources: Bloomberg